Australian cattle prices remain at premium to global competitors

Global cattle prices remain disjointed, with a variety of supply and demand factors influencing sharp price movements throughout the year, according to Meat & Livestock Australia. 25 December 2020

25 December 2020

3 minute read

3 minute read

The rising number of COVID-19 cases in the US, dry conditions in South America and the shift in seasonal conditions across Australia remain key influences on cattle prices at present.

Earlier this year, when rainfall prompted a turn in the season, Australian cattle prices spiked as producers looked to replenish supply levels following the long period of elevated turnoff. This has flowed into restocker categories across Australia remaining elevated over their feeder and processor counterparts to sit at record levels as demand for cattle heats up.

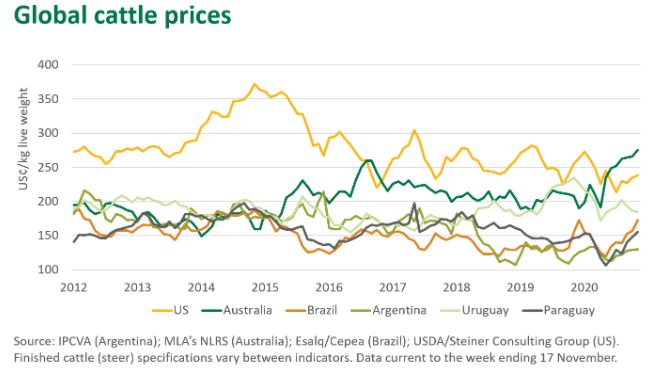

Typically, Australian prices tend to align with Uruguay and remain below US levels, however, Australian cattle prices have been the highest in the world since June. In September, the price of Australian beef jumped up to US$6.76/kg, a rise of 11% on the month prior and well above the average 2019 price of US$5.74/kg. Through November, Australian cattle prices have maintained a 16% premium over US counterparts.

The high price of Australian cattle will place pressure on the affordability of Australian beef across markets and could lead to importers looking to other suppliers for more cost-effective options. If the premium on Australian beef becomes a barrier for trade, prices will likely ease across time.

US market conditions remain unsettled

Earlier in the year, when US processor capacity dropped off as COVID-19 cases spiked, US cattle prices fell away as demand disappeared. Since then, as market conditions stabilised, prices have steadied. Leading into the US Thanksgiving holiday period, recent demand for beef has been solid, further supporting cattle prices, particularly as wholesalers look to build some inventories and prepare for potential supply disruptions associated with the recent surge in COVID-19 cases. A number of US states have already reduced indoor dining capacity, creating uncertainty for sit-down restaurants, in particular.

With supplies from Australia and New Zealand remaining tight, the US imported 90CL indicator has lifted 7% on the same week last month to reach US217¢/kg. Last week, Steiner Consulting reported that given the tight beef supplies from Oceania, imported trim will likely continue to trade at a short-term premium to its US domestic counterpart.

Dry conditions across South America

South America continues to struggle with dry conditions across the region. In Brazil, cattle prices have been rising as slaughter levels begin to tighten after two years of drought – cattle slaughter contracted 11% in Q3 2020 relative to Q3 2019. With Chinese demand for Brazilian beef escalating through the year, this has had a strong upwards influence on Brazilian cattle prices. Brazilian meatpackers are expected to reduce their capacity in order to adapt to the reduction in cattle supply, which could level off the rise in prices.

From a percentage perspective, the rise in Brazilian cattle prices has been comparable to Australian price movements. When considering the volatility of markets through 2020, this lift in prices across the two largest global suppliers of beef could come as a shock for import markets.

Australia maintains position as world’s second largest beef exporter

Moving forward, Australia will continue to play an important role in the global beef trade. For FY2019–20, Australia accounted for 17% of global beef exports across a diverse range of destinations, playing a pivotal role in ensuring food security for many nations around the world. While the price point may be shifting, demand for Australian beef will remain, underpinned by strong fundamentals such as Australia’s reputation for quality, consistency and safety.

TheCattleSite News Desk