US Cattle Inventory Down Mid-Year

US - Only a vague picture of cattle inventory status can be given at the current time, but data available suggests further contractions, according to Derrell Peel of Oklahoma State Universtiy and James Robb and Katelyn McCullock of the Livestock Marketing Information Centre. 8 August 2013

8 August 2013

3 minute read

3 minute read

The status of cattle inventories in the U.S. is unknown at this time. USDA’s National Agricultural Statistics Service cancelled the report mid-year report, so there are no official July 1 survey-based estimates of cattle inventories by class, 2013 calf crop, or total Cattle on Feed available.

At the recent annual meeting of the Technical Advisory Committee of the Livestock Marketing Information Center (LMIC), members from around the country were polled as to their expectations for the beef cow herd and beef replacement heifer situation in their region. Nationally and by region, the group was unanimous that the beef cow herd is down so far this year, with the U.S. assessments ranging from less than one percent to over two percent.

The majority of the group indicated that the beef cow herd was likely down between one and two percent as of July 1. Assessments on beef replacement heifers was more variable with some limited view that modest heifer retention was occurring in some areas with a majority feeling that no significant heifer retention was occurring yet or that some heifers earlier retained for breeding had been diverted into feeder supplies.

Based on member input and other available data, the LMIC has developed estimates in the format of previous July 1 inventory reports. It is important to remember that these estimates do not reflect USDA survey and statistical methodology and should not be viewed as a replacement for official estimates.

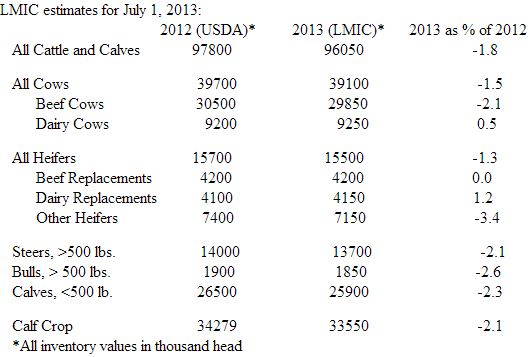

These estimates reflect indications from various data that are available and historical relationships; importantly they started with a baseline of the July 1, 2012 mid-year report. The only category posting any year-on-year increase was the number of dairy cows. All cattle and cows as of July 1st were likely down between one and two percent. Beef cows likely dropped just over two percent, resulting in reductions for seven consecutive years.

Beef cow slaughter was down 3.1 percent year-over-year in the first half of 2013. Beef cow slaughter has fallen sharply in the past three weeks and

is likely to be down for most of the remainder of the year. The number of heifers on feed usually decreases between January and July and was down this year but dropped less than normal indicating that some animals previously identified as replacements likely entered feedlots in the first six months of this year.

Heifer slaughter is down year to date but has been above year ago levels in the last four weeks, indicating the larger number of heifers finishing in feedlots, according to Oklahoma Cooperative Extension Service.

Heifer retention may well pick up in the last half of the year. Still, the combined effects of higher beef cow slaughter and decreased heifers entering the herd likely means that the beef cow herd will be down year-over-year on January 1, 2014

The lack of USDA mid-year inventory estimates prevents the usual calculations of estimated feeder supplies outside feedlots. However, using the LMIC estimates above along with additional assumptions about the total U.S. cattle on feed inventory as of July 1, suggests that feeder supplies were down fully two percent year-on-year. This estimate factors in a smaller 2013 calf crop and reduced feeder cattle imports in 2013. Renewed heifer retention interest in the last half of this year could squeeze feeder supplies dramatically in 2014.

The Markets

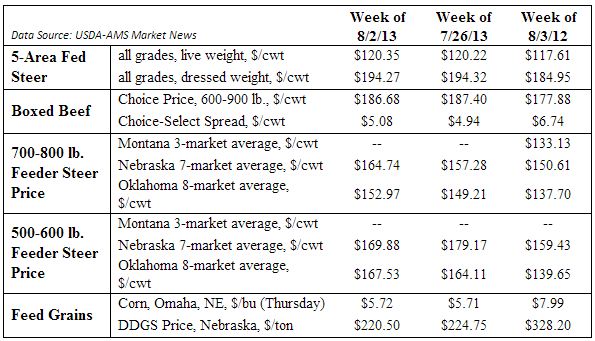

Fed cattle prices were steady with the prior week and nearly $3.00 per cwt. above a year ago. Wholesale beef prices (boxed beef) drifted slightly lower during the week. As a result, beef packer margins continued to erode seasonally.

Calf and yearling prices remained solidly above 2012’s, supported by year-on-year declines in feedstuff costs. Some calf markets posted weekly declines, including Nebraska.